As countries begin to emphasize their semiconductor industry, the semiconductor industry has been developing rapidly in recent years, and in 2021, the overall market growth rate reached 26.2%. However, with the impact of global economic issues, trade issues and geopolitical factors this year, the semiconductor market development rate has begun to slow down, and it is expected that the overall rate of increase will be around 4% in 2022, with the overall market size reaching 620 billion U.S. dollars. The overall market size is expected to reach 620 billion U.S. dollars in 2022, with an overall increase of about 41 TP3T.

As global inflation continues to deepen, consumers have begun to reprioritize their discretionary spending, including lower spending on travel, leisure and entertainment, which has had an impact on the semiconductor industry. Recently, a number of market research organizations have begun to issue warnings that the global semiconductor market will begin to grow negatively in 2023, implying that the market has fallen into contraction for the first time after three consecutive years of positive growth.

Multiple Organizations Issuing Early Warnings

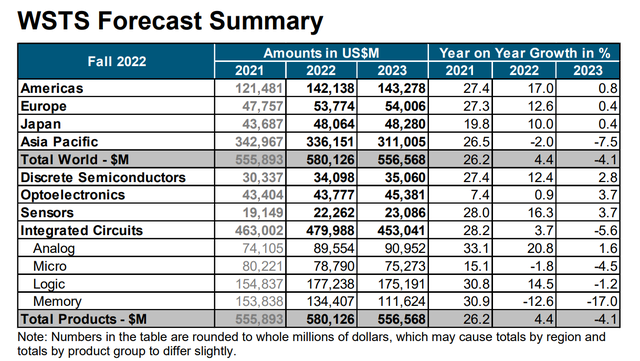

Recently, by the world's major semiconductor manufacturers of the World Semiconductor Trade Statistics Organization (WSTS) released the latest report, is expected to 2023 semiconductor market size will be reduced year-on-year by 4.1%, down to 556.5 billion U.S. dollars, which is not the first time the WSTS released a forecast report in 2023.

Back in the spring of this year, WSTS had forecast an overall market growth rate of 5.1% for 2023, but by August, the organization had lowered this expectation to 4.6%, and this time it has again significantly lowered its forecast, which can be considered as not optimistic about the market next year. Special attention is paid to the WSTS as a global semiconductor supply and demand trends research organization, which includes more than 40 members of the global semiconductor companies, such as Samsung Electronics, SK Hynix, TSMC, Micron, etc., can be considered to be based on the movements of these companies, the industry as a whole to make judgments.

Not only WSTS, the latest forecast from research firm Gartner shows that global semiconductor revenues are expected to decline by 3.6% in 2023. In response to this Gartner's practice vice president Richard Gordon said that the short-term outlook for semiconductor revenues has worsened, and that the rapid deterioration of the global economy as well as weakening consumer demand will have a negative impact on the semiconductor market in 2023. The rapid deterioration of the global economy and weakening consumer demand will have a negative impact on the semiconductor market in 2023.

Meanwhile, the semiconductor market has been polarized between consumer-driven and corporate-driven markets. The weakness in the consumer-driven market is mainly due to inflation and falling disposable incomes as a result of rising interest rates, which has led to weak demand for consumer electronics.

And enterprise-driven markets such as enterprise networking, enterprise computing, industrial, healthcare and commercial transportation remain relatively resilient despite the ongoing macroeconomic slowdown.

IC Insights, another leading industry organization, released a similar view that global semiconductor sales will decline by 5% in 2023, and that the adverse conditions that hampered semiconductor sales in the second half of 2022 are expected to continue into the first half of next year.

IC Insights attributes the lower sales to a combination of factors, including the current global economic slowdown, weak demand for computers and smartphones, rising wafer inventory levels, and continued weakness in the memory IC market.

Of course, because the semiconductor market is always cyclical characteristics, the report that in 2023 after the market decline, the following three years will be a stronger growth, is expected to 2026, semiconductor sales will climb to 8436 billion U.S. dollars, the annual compound growth rate of 6.5%.

Computer memory is the first to bear the brunt, analog devices, sensors, discrete devices still have opportunities

From the reports of several organizations, it can be seen that at the beginning of this year, most of them were still optimistic about the semiconductor market in 2023. However, under the influence of the global macro-economy and the weak demand in the consumer market, various organizations have downgraded their expectations to negative growth. Obviously, the market is shrinking beyond expectation, and enterprises have to be prepared to meet the downturn of the industry.

Overall, the main reason for the decline in semiconductor sales in 2023 is that the memory chip market is facing tremendous difficulties. On the one hand, demand for computer memory will decrease due to weak demand in the PC and smartphone markets. On the other hand, although the server market is relatively stable, reduced investment by related enterprises and the de-stocking of lower-end customers will also affect demand in the second half of the year.

In the third quarter of this year, world-renowned memory chip makers such as Micron, SK Hynix, and CAYIN have announced that they will cut capital expenditures or wafer production. SK Hynix has announced that it will cut next year's capital expenditure program by half, while Micron and CAYIN have indicated that they will cut their spending on memory devices by 20% to 30%.

Previously, IC Insights published a report showing that the semiconductor market was expected to reach $190.4 billion in capital expenditures this year, a year-over-year increase of $24%. However, a recent revision has lowered the forecast to $19%, with capital expenditures at $181.7 billion. Nevertheless, the revised capex forecast is still at an all-time high.

Semiconductor capital expenditures grew by 101 TP3T in 2020 and rose sharply by 351 TP3T in 2021. If the industry's capital expenditures grow by 191 TP3T this year as projected, it would mean that the industry would once again see three years of double-digit capital expenditures growth since 1993-1995. The main reason for this year's downward revision in capex is the weak memory market.

In terms of market size, the memory market is expected to remain flat in 2022 and decline by 16.21 TP3T YoY in 2023 amidst persistent weak demand, swelling inventories, and customers starting to keep prices down.

Taking DRAM as an example, according to Gartner analysts, global DRAM revenues will decline by 2.61 TP3T in 2022 to reach US$90.5 billion, and will further decline to 181 TP3T in 2023, reducing the market size to US$74.2 billion.

The Gartner report also pointed out that in the NAND market, the rapidly deteriorating demand environment was somewhat masked by numerous NAND fab shutdowns in the first quarter of this year that raised prices, leading to excess inventory in the third quarter, a situation that is expected to continue into the first half of 2023. NAND revenues are expected to grow by 4.4% in 2022 to reach US$68.8bn, but will decline by 13.7% in 2023, reducing the market size to US$59.4bn.

J.P. Morgan, Nomura and other leading global brokerage firms have also issued warnings that the first half of next year will not be optimistic for the memory industry, with prices set to plummet by as much as 50%. However, Citi analysts believe that this pessimistic outlook is unlikely to last for long, although the growth in memory shipments is likely to slow down in the next few quarters. The memory market is expected to reach its nadir in the first half of 2023 and begin to recover in the second half of 2023.

In addition to memory, logic chips such as Display Driver ICs (DDIs) used in smartphones and TVs are expected to see sales drop by 1.2% next year after achieving a high growth rate of 14.5% this year.

However, in addition to the decline in the memory and logic IC markets, there are still some semiconductor products that can continue to maintain the upward trend. Among them, analog chips are expected to grow by 20.8% this year, and the growth rate is expected to narrow to 1.6% next year, while other semiconductor products, such as discrete devices, sensors, and optoelectronic chips, are expected to grow by 2.8%, 3.7%, and 3.7% next year.

Trivia

At present, various organizations have downgraded next year's semiconductor sales market expectations, on the one hand, in the continuing impact of macroeconomic factors, as well as inflation led to a decline in consumer demand; on the other hand, due to the semiconductor market in the last three years, the continued high investment, along with the release of capacity, so that the market began to start from the supply does not meet the demand to the supply over demand, which is the most affected by the memory market. However, some organizations believe that the contraction of the semiconductor market is only temporary, with the recovery of the market and the development of technology, the semiconductor market will be back out of the more powerful rally.

Watch Honghong share more new knowledge about the industry >> What's New in Honghong Real Estate

Source. Audiophile